|

With ridesharing services like Uber and Lyft, now anyone with a smartphone can become a driver for hire where, instead of flagging down the car like a passing taxi, customers use a mobile app to request and pay for a ride.

But here’s the catch. Since many of the drivers who work for ridesharing companies do not have a livery driver’s license and their cars are neither registered nor insured as commercial vehicles, it creates an insurance gap, or a period of time when they are underinsured and taking on more financial risk. Companies like Uber and Lyft are called a Transportation Network Company (TNC) and there are different coverage periods for these drivers. If you drive for a TNC, make sure you know the three distinct coverage periods and the insurance coverage you need at each time. Period one: The app is turned on and the driver is waiting for a fare. Period two: The fare has been accepted and the driver is on the way to pick up the passenger. Period three: The passenger is in the car. Right now, TNCs only provide full coverage in periods two and three, meaning drivers are likely to be underinsured during period one, which begins the moment they turn on the app, but before they accept a fare. And some drivers may not be aware of this gap in insurance coverage. If there is an accident during period one, the driver may be on the hook to cover the cost of some liability damages and have no coverage to repair their vehicle. Different ridesharing companies have different coverages during this period, so adding a specific rideshare gap endorsement onto their personal auto insurance policy could keep the driver fully insured. If you’re thinking about driving for a TNC, ask what level of coverage it provides during each period. Drivers should also contact their own auto insurer to address gaps, if any, in their liability protection. It is also recommended that TNC drivers review a copy of their TNC’s insurance contracts so they know the exact terms and conditions of the coverage. Knowing your insurance needs as a ridesharing driver doesn’t have to be complicated. Your local independent agent can help guide you through it and make sure you have the insurance protection you need. Grange Insurance offers ridesharing gap coverage that enables TNC drivers to fill in their gaps in coverage. If insurance policy coverage descriptions in this article conflict with the language in the policy, the language in the policy applies. To learn more about Grange’s ridesharing gap coverage, speak with your independent Grange agent. Reference: - Insurance Information Institute - https://www.grangeinsurance.com/tips/drive-for-uber-lyft-mind-your-insurance-gap

0 Comments

By Steve Temple, automedia.com Today's two-part urethane paints consist of a clear coat on top of the color coat. While this system preserves the color by protecting against UV rays and provides a brighter shine, it can also get scratched fairly easily. Just rubbing your rag on a dusty surface, or having grit in the cloth itself, can leave fine lines and swirls. Visible lines If polishing and waxing isn't producing the smooth finish you'd like to see on your vehicle, but you can't feel the scratches with your fingernail, then a simple liquid scratch remover might do the trick. Note, however, that not all car scratches are the same. Some marks may be due to rubbing against a bumper from a car or shopping cart. The material coming into contact with your finish might be softer, and simply leaving behind a bit of material on top of the paint. If that's the case, it may come off easily with a spray for removing tar, bugs and adhesives. Be sure to use a product specifically designed for marks on paint, as acetone or types of solvents might damage the paint. If the mark is still there after using the spray cleaner, try using a soft-grade rubbing compound (it's easy to penetrate the clear coat, so don't overdo it). You'll need to use a polishing compound to remove any fine scratches left by the rubbing compound, and then finish the job by sealing the surface with a good car wax. Medium-depth scratches that you can feel with your fingernail require a more aggressive method of repair than simply using rubbing and polishing compounds. Bad scratches that penetrate to the color coat can require touch-up paint and possibly professional care. Smooth operator For the medium-depth scratches, use a car scratch remover kit. The system is fairly easy to use, requiring three separate steps and a common household drill. As with the rubbing compound mentioned above, less is more. The idea is to take off a very thin layer of the clear coat, but still leave enough on to protect the paint. And you'll need to protect the finish with a good wax or synthetic polish to bring back the shine. Scratch removal tips

Source: https://mobiloil.com/en/article/car-maintenance/basic-car-maintenance-tips/car-scratch-removal?stat=318514&socialnet=preview By: April Daniels

As an independent agent one of the most commonly used phrases when talking about auto insurance is “full coverage.” If you have a vehicle with a loan you need “full coverage”? Does “full coverage” mean you have towing? What deductibles are included in “full coverage”? The problem with that phrase is that it means something different to each individual person! What I prefer to do at Belt Insurance is to break down your coverages by categories and make sure that you have the best coverage in each category.

So, after reading this here is a quiz for you! I’m going to list two customers coverages on their 2015 Ford Focus and you tell me if they have “full coverage” or not. Customer A

Customer B

Now these customers both vary in the amount of coverage they have on their policy, but they could both consider their policies on “full coverage.” It’s important to remember that almost all coverages are optional and can change to your preference. If you have questions about your coverage or want to know more about what you pay for every month call your local agent. We will be happy to assist you in explaining coverages and give you different costs associated with adjusting them! How much does your lifestyle influence your car insurance?

Answer: Quite a bit. Having the right auto insurance can be just as important as having auto insurance at all. Depending on your lifestyle, you may have unique coverage needs to protect the people and things that are important to you. And your needs can change throughout your life. So, whether you drive a semi-autonomous vehicle or a classic auto, have a baby or a puppy on board or spend your day driving an All-Terrain Vehicle (ATV) or a minivan, make sure your auto insurance fits your lifestyle when purchasing an insurance policy. If you are a Tech Wiz, then consider:

If you're a Parent, then consider:

If you are an Adventurer, then consider:

If you are an Eco Advocate, then consider:

If you are a Semi-Professional or Professional Driver, then consider:

And everyone should think about:

And as your lifestyle changes, your coverage needs may change, too. Keep your agent informed so you have the right coverages for every stage in your life. There are many online tools to help you consider the kinds of questions to ask your agent, such as Insure U’s Life Stages tool or Ohio Department of Insurance’s Auto Insurance Toolkit. Grange Insurance offers PinPoint Auto® personal auto insurance coverage that’s customizable to your lifestyle, budget and coverage needs. Talk to a local independent Grange agent for details on coverages and discounts. If the policy coverage descriptions in this article conflict with the language in the policy, the language in the policy applies. Coverages described above may not be available in all states. Policies underwritten by Trustgard Insurance Company, Grange Indemnity Insurance Co, Grange Mutual Casualty Company, Grange Life, Grange of Michigan*, Grange Property and Casualty*. All companies are members of the Grange Mutual Casualty Group. WE RESERVE THE RIGHT TO REFUSE TO QUOTE ANY INDIVIDUAL PREMIUM RATE FOR THE INSURANCE HEREIN ADVERTISED. *Not licensed in Pennsylvania. Reference: - Insurance Information Institute -https://www.grangeinsurance.com/tips/matching-car-insurance-to-your-lifestyle?utm_source=grangewire&utm_medium=email&utm_campaign=tips&utm_content=71217 Will you marry me?

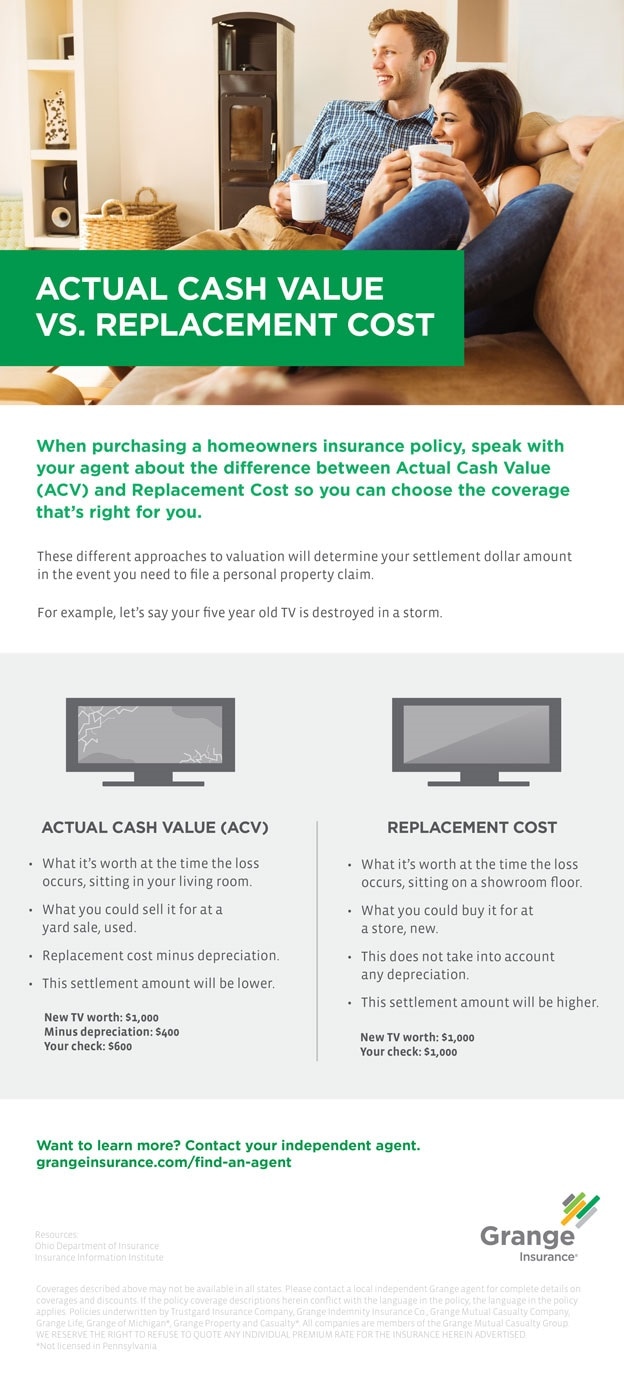

No matter how you say it, asking someone to marry you is a huge step in your life and can come with some pre-proposal jitters. Not to add any more stress—but have you thought about what you would do if something happened to the ring? What if you lost it? Or it got damaged? And if that doesn’t make you nervous, think of the reaction of your soon-to-be fiancée when the ring is missing or broken, which could potentially cost thousands of dollars to fix or replace. According to the Insurance Information Institute, jewelry losses are among the most frequent of all homeowners’ content-related insurance claims, so these scenarios aren’t far-fetched. The best way to protect your high-value, sentimental jewelry is with insurance. Take a look at our quick guide to purchasing insurance for your engagement ring, and give your agent a call so that when you promise, “till death do us part,” you can ensure the same for the ring. Step #1: Buy the ring and keep the receipt. Your insurance carrier may require the retail value of the ring before providing coverage, so hang on to your receipt. Step #2: Call your independent agent. Your independent insurance agent will guide you through this process including walking you through your options, helping you choose the best policy, and hopefully easing some of your nerves since you can rest assured that the ring will be protected. Step #3: Get an appraisal. Your independent agent can help you determine if an appraisal is needed. While a receipt is sufficient for many rings, for more expensive jewelry, your insurer may require an appraisal. The appraisal will examine all diamonds and other stones, as well as the band, to determine the value of the ring, regardless of how much you paid for it. You may also be asked to get an appraisal if the ring is an antique or family heirloom. Step #4: Raise your limits or add an endorsement. When insuring your ring, you have two options: raise your limits or schedule the ring as an endorsement. Homeowners and renters insurance policies include coverage for the contents of your home. However, a base homeowners policy typically limits theft of jewelry coverage up to $1,000, or sometimes just $500. Because of this, simply boosting your limits may not be enough to cover your fiancée’s new bling. Scheduling the ring as an endorsement is another option. Although it may increase your policy’s premium cost, it provides coverage for a broader spectrum of losses. And your policy deductible doesn’t apply; this means that you could replace the ring at no additional cost to you. When debating how to insure the ring, use your independent insurance agent as an expert resource to help you choose the best coverage for you. Step #5: Propose! Confidently pop the question, knowing that if the ring accidentally gets trampled in the midst of your proposal flash mob, tumbles down the stadium seats as your engagement is broadcasted on the jumbotron, or even if your fiancée finishes the slice of cake and never quite finds the ring inside… you’re covered. Please contact a local independent Grange agent for complete details on coverages and discounts. References - Brides.com - Insurance Information Institute -https://www.grangeinsurance.com/tips/guide-to-engagement-ring-insurance Actual cash value vs. replacement cost: Which one’s best for you?Posted in Home Imagine this situation. About five years ago, you bought a new flat screen TV for over $1,000. Then after a thunderstorm rolls through, it won’t turn on. It’s destroyed. So, you file a claim with your insurance company, but you’re left confused when your settlement check is less than $1,000. After all, that’s what you paid for the TV, right? It all comes down to the type of contents coverage you’ve selected in your homeowners insurance policy: actual cash value or replacement cost value. But you can avoid this confusing situation by reviewing your coverage options with your independent insurance agent ahead of time. Check out our infographic about actual cash value and replacement cost to help you understand the difference so you can choose the right coverage for your home insurance policy.  You may be frustrated with car insurance premiums and factors that cause increases, such as:

COPYRIGHT: Insurance Publishing Plus, Inc. 2014 All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc. Do you need flood insurance? Well, walk to the nearest mirror and ask the person you see if he or she owns much property that could be damaged or destroyed by water. If the answer is yes, then you should seriously consider buying flood insurance. Most persons who need the protection buy coverage offered by the National Flood Insurance Program (NFIP). If your community doesn't participate in the program, you'll have to look into coverage from private insurance companies.

Is A Flood Loss Likely? The chances of your business, home or personal property being damaged by a flood depends primarily upon where you live. They also depend on other factors such as: · how much of a flood warning you receive · the level of flood precautions you take (such as moving personal property from lower levels to higher levels), and · the precautions taken by your community (such as the use of flood controls in construction standards or sandbagging threatened areas). Floods are related to weather conditions and tend to affect very wide areas. This often makes chances of a flood loss higher than a loss from fires or windstorms. Many people have the obsolete belief that flood insurance is only needed if you live in a flood prone area. I Live In A Flood Zone?! If you hear the term "flood zone," you may think that it refers to locations that are particularly vulnerable to flooding. Wherever you live in the USA, you live in a flood zone. While your area may have a lower chance of flooding than a coastal area or a location situated near a body of water, your area could still experience flooding. A very dry part of the country can be susceptible to flash floods; hilly locations may be harmed by drainage; snowy locations may suffer from heavy snow thaw; other areas may suffer deluges or flooding due to a heavy rain season which has soaked the surrounding soil. So, if you've insured yourself against fire, wind and other causes of loss, it certainly makes sense to also protect yourself from the potential of a flood loss. Why Worry When Disaster Coverage Is Available? Are you thinking that, after a flood, your loss may be handled by the government declaring a disaster area? However, you're still taking a couple of large risks. First, your flooded locale may not be deemed a disaster area. Second, being designated as a disaster area is not a bargain. Disaster area status only gives citizens access to government disaster loans. IF you qualify for assistance, you have replaced insurance protection with an obligation to pay off a large, long-term loan. Is it worthwhile to gamble on an opportunity to pick up more debt? You'll find flood insurance to be a cheaper and much more valuable alternative. Don't Be "All Wet" You don't have to leave yourself unprotected. Your agent, an insurance professional, can help you with detailed information on the National Flood Insurance Program. You can also ask for help in getting the coverage you need in the face of a flood. COPYRIGHT: Insurance Publishing Plus, Inc. 2014 All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc. People are renters for different reasons. Regardless whether it is because of financial necessity or a lifestyle preference, renters frequently choose not to insure for reasons such as:

The only thing true about the above reasons for not getting renters insurance is that they can cause real misery from an uninsured loss. Renters need to consider the following:

Renters who don't carry insurance should remember that they also need protection for their legal obligations to others. What if you're on a softball team with your friends and you smash a line drive into the face of another player? Emergency treatment and cosmetic surgery is expensive. If you rent and you don't have insurance…then you have a very good reason for contacting an insurance professional to get you covered….now! COPYRIGHT: Insurance Publishing Plus, Inc. 2016 All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc. If you own and/or run a smaller business, your insurance needs may be properly handled by a businessowner policy (BOP). A BOP is a single form that offers both property and liability protection. Retailers, wholesalers, small contractors, artisan contractors, dry cleaners, restaurants, offices and convenience stores (including those with gas pumps) are eligible for BOP coverage. All such operations may be insured by a BOP as long as they do not exceed the square foot or annual sales limits established for the program. Cooking operations, due to the higher fire and other accident exposures, have significantly more restrictive guidelines.

Property Coverage - BOPs protect buildings as well as the following: -building additions (completed or being built) -indoor and outdoor fixtures -clothes dryers -machinery and equipment -landlord furnishings, -mowers, ladder, snow blowers, and similar maintenance property -outdoor furniture -floor coverings -refrigerating appliances -ventilating appliances -cooking appliances -dishwashing/drying appliances -clothes washers -materials, equipment, and supplies -temporary structures located near the insured premises The policy's protection for business personal property (such as office equipment, copiers, desks, etc.) applies whether the property is located inside or immediately outside the covered buildings. The category also includes property you own, lease or control (i.e., borrow or control) as long as the property is used by the business. Liability Coverage - A BOP’s liability coverage provides comprehensive protection for claims or suits made by other parties. Specifically it covers losses involving injury to other persons or damage to property that belongs to others. It also provides limited protection against personal injury (slander or libel), advertising injury and losses involving an operation's products or services. Naturally, there are certain situations that are not covered by a BOP. For instance, there is no coverage for losses involving most vehicles, money and securities; illegal property (contraband), land, water, growing crops or lawns; or watercraft. Enhancing Coverage - A BOP may be supplemented to provide additional protection. Property coverage options include adding insurance for accounts receivable, valuable papers and records, earthquake, spoilage, etc. Liability coverage can be expanded to handle additional business interests, limited vehicle liability, losses related to personnel situations, liquor liability and injuries to leased employees. A BOP may be the answer to your company's coverage needs and it may be worthwhile to get more information on the BOP from the nearest insurance professional. COPYRIGHT: Insurance Publishing Plus, Inc. 2014 All rights reserved. Production or distribution, whether in whole or in part, in any form of media or language; and no matter what country, state or territory, is expressly forbidden without written consent of Insurance Publishing Plus, Inc. |

Navigation |

Connect With Us |

Contact Us |

Location |